A record number of new and huge container ships will hit the water in 2023

A record number of new and huge container ships will hit the water in 2023

There’s a high possibility of an all-out price war in the container shipping and liner industry, which will be hit by other volatilities like inflation, the implications of the war on Ukraine, the impact of Covid-19 in China, and worker strikes in the current year.

The predictions have been made by the online container logistics platform Container xChange, which has published the Container LogTech predictions report for 2023, highlighting important global trends facing the shipping and supply chain industry in 2023.

The year 2022 was all about tight capacity and exceptionally high container rates. Towards the latter half of the year, the prices started to plummet and continue to crash as we transition into the new year, according to the market forecaster issued by Container xChange, the online container logistics platform.

|

|

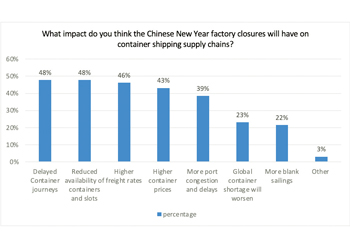

Congestion at depots is expected to stay throughout Q1 |

There is significant market volatility that continues to disrupt the container shipping industry. With a significant oversupply of containers and a further influx of more TEUs in 2023, shipping lines continue to reduce vessel capacity and suspend services by considerable blank sailings. In a recent advisory, Maersk indicates that it will continue to ‘make capacity adjustments on services from Asia to North America, Europe and the Mediterranean to better align with demand fluctuations.’ We observe a similar trend echoing in the industry.

“In 2023, there is a high possibility of an all-out price war. It doesn’t seem that the capacity restrictions that we have seen in the past two years are due to return, so we’ll just have ample capacity both on the vessel as well as on the container side. With the competitive dynamics in the container shipping and liner industry, I don’t expect especially the big players to hold back, and we do expect prices to come down to almost variable costs. We also foresee market consolidation,” said Christian Roeloffs, Cofounder and CEO, of Container xChange, an online platform for container logistics.

This is starting with initially carriers defaulting and reducing their fleet. Recently, there was news about China United Lines, an emerging carrier on transpacific and Asia-Europe services, being at risk of defaulting on a charter party involving more than 10 containerships.

“Into the year 2023, freight forwarders will be able to go window shopping quite a lot, and there’s going to be a lot of room for negotiation, especially in the early parts of the year. Contract rates will follow suit as spot rates fall significantly,” Roeloffs added.

He further said that we will continue to see efforts towards diversification of supply chain sourcing and manufacturing out of China. This is a long-term view, and it will need vision and strategy from companies looking for a more resilient supply chain.

Besides, the economies will also witness increased container volumes intra-Asia and more countries will emerge as potential alternatives like Vietnam, India and more.

In such an environment where there will be tighter margins for freight forwarders and traders, the cost is going to be everything. Leaders will look for ways to efficiency and business sustenance.

Further, technology offers a great opportunity for leaders to minimise risk with data visibility and transparency while also maintaining a healthy partner portfolio that helps greatly in testing times, Roeloffs added.

“Tight grip on costs becomes paramount for freight forwarders into the year 2023. While on one hand there will be a great deal of negotiation with shipping lines and on the other hand, operational cost optimisation will be crucial for the forwarders. There will be careful monitoring of the demurrage and detention charges, for instance, insurance charges, claims etc. As capacity on the ocean side becomes more abundant, there is a valid business case for using SOCs which not just offer flexibility but greater control to the forwarders,” said Dr Johannes Schlingmeier, cofounder and CEO, Container xChange.

To think of the situation from a more macro-lens, it seems that what we experienced in the past three years is a natural reaction of market forces of demand and supply resulting from the disruptions like covid-19 and subsequent lockdowns, the war in Ukraine by Russia, geopolitical risks and many more. Container prices skyrocketed soon after the pandemic hit because there were not enough containers to fulfil the rising demand and that’s when retailers and importers started to stock much more in advance to avoid the historic port congestions.

The pre-peak season in 2022 saw record container throughput in import-heavy ports. Now that the stocks have been filled, the demand is plummeting. Inflation and the energy crisis are leading up to cautious spending which will have its own impact on the container industry. The shipping industry will survive this, and we will again start to see normal activity levels in the future, though not immediate future. The good part is, that the worst is behind us.