The study chart

The study chart

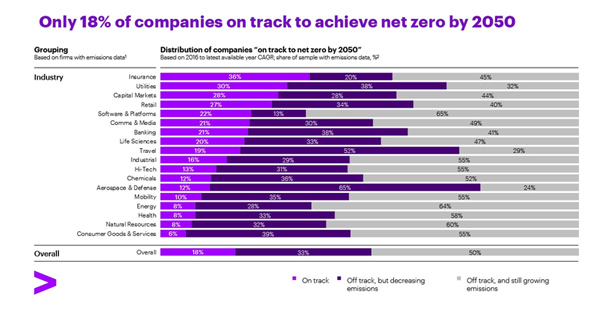

Fewer than one in five firms (18%) are on track to reach net zero emissions in their operations by 2050, and over a third (38%) say they cannot make further investments in decarbonisation in the current economic environment.

This is according to new research from Accenture, a leading global professional services company.

However, industry leaders can break this economic stalemate within only three years by reinventing decarbonisation strategies that enable growth for energy-intensive, hard-to-abate heavy industry—such as steel, metals and mining, cement, chemicals and freight and logistics—the operations of which generate 40% of total global CO2 emissions.

2,000 largest companies

Released ahead of the 28th UN Climate Change Conference of the Parties (COP28), the research analyses net zero commitments, decarbonisation activities and emissions data for the 2,000 largest companies globally. Additional primary research includes a survey of more than 1,000 executives across 14 industries and 16 countries to understand the near-term challenges and priorities of industrial decarbonisation.

Accenture’s analysis in Destination net zero found the number of companies that have set targets for net zero has risen to 37%, up from 34% last year. Despite reason for tempered optimism, half (49.6%) of the companies that disclose emissions data have presided over increasing emissions since 2016.

One-third (32.5%) are cutting emissions, but on current observable trends are not on track to reach net-zero in their operations by 2050. To address the issue at an enterprise level, the report identifies a broad set of decarbonisation levers that enable and accelerate progress.

Decarbonisation levers

These range from well-established actions, such as improving energy efficiency and switching to renewables, to more complex measures, such as the implementation of green IT, the reinvention of business models and carbon removal.

“It’s promising to see an increase in public commitments to net zero targets again this year, but the adoption of key decarbonisation measures is not uniform, with some companies still unable to master the basics,” said Jean-Marc Ollagnier, CEO of Accenture for Europe, Middle East and Africa.

“Reaching net zero is a unique opportunity for every organisation to reinvent themselves and their value chains by aligning business growth with the net zero imperative, despite the many obstacles they must overcome. However, it is not just an enterprise challenge but also an ecosystem one, as there is a need to address the disconnect between supply and demand.”

When surveying leaders for the Powered for change report, Accenture found that heavy industry reinvention is critical to achieving all global net zero targets—both as the world’s biggest emitters and due to their interdependence with manufacturing, or “light” industry, which includes pulp and paper, aerospace and defense, automotive, industrial equipment, life sciences and consumer goods. However, economics of decarbonisation and structural misalignment between industries are at the core of what’s constraining progress:

•Improved access and availability to affordable, low-carbon energy is required: Four out of five (81%) leaders from heavy industry expect to need more than 20 years to have sufficient zero-carbon electricity to decarbonise their industry, with energy providers primarily focused on decarbonising their own operations.

•There is a need to bolster confidence in the commercial viability of low-carbon products: 95% of heavy industry leaders expect to need at least 20 years to deliver net zero products or services at or close to price parity with high-carbon alternatives, and just over half (54%) say that manufacturers' future purchasing intentions give them enough confidence to invest in decarbonisation.

•Concerns about managing the costs must be addressed: Two in five (40%) leaders in heavy sectors said they can't afford further investment in decarbonisation in the current economic climate, with 63% suggesting their priority decarbonisation measures won’t be economically attractive before 2030.

Collective action

“The rapid, affordable decarbonisation of heavy industry requires collective action across the value chain and urgently compressed transformation. We believe this can break the economic stalemate by inspiring new levels of growth and help accelerate net zero in just three years of focus,” said Stephanie Jamison, global resources industry practice lead and global sustainability services lead at Accenture. “If heavy industry is burdened with the full cost of decarbonisation and fails to meet net zero targets, all industries will fail.”

Most organisations use a three-year strategic planning cycle, and while three years will not be enough to fully achieve net zero for most, the report lays out what must be accomplished during this crucial timeframe to eliminate the economic growth trade-offs and advance net zero. To build this foundation, three key steps must be taken within the next three years for viable decarbonisation pathways that simultaneously pull on as many decarbonisation levers as possible:

Target green premiums to finance the first phase of industrial decarbonisation: Light industry must lead in this initiative. Absorbing upfront costs of decarbonisation and knowing which green products to target are key to unlocking future savings. In fact, 52% of executives in heavy sectors view revenue growth as the primary path to improving the economic business case for the top three decarbonisation priorities.

Scale low-carbon power and hydrogen more quickly to guarantee affordable, secure supply: Accenture projects the levelised costs of solar power and green hydrogen could fall by 77% and 74% by 2050, respectively, if their potential is optimised, ultimately reducing green industrial products’ costs. Additionally, almost two-thirds (64%) of oil, gas and power companies believe their industrial and logistics customers are willing to enter long-term decarbonisation partnerships, collaborating to initiate a virtuous circle.

Drive down the capital and operating expense related to low carbon infrastructure: It is essential that cost reductions, which are mostly in the control of heavy industry, are fully realised to drive their decarbonisation. For example, based on our analysis, there is significant cost reduction potential (49% by 2050) in green steel, with reduction in construction and equipment costs a key lever.

Jamison added: “To provide the business growth that is necessary to put net zero back within reach, these imperatives must be executed in parallel and scaled to meet the moment, starting right now. Stakeholders around the world—across industries and governments—must come together to create a new frontier for the economics of decarbonisation, giving heavy industry a firm foundation for reinvention.”--TradeArabia News Service